Why Your Default Pension Fund Is Probably Wrong for You

Most people never choose where their pension is invested. They're placed into a default fund designed for everyone — which means it's designed for no one. Here's why that matters.

The Best Reform in a Generation — With a Built-In Flaw

Auto-enrolment is arguably the most important thing the government has done for pensions in decades. Before it was introduced under the Pensions Act 2008 and rolled out from 2012, millions of private-sector workers had no pension at all. Participation in workplace pensions had been falling for years — from around 55% of employees in 1997 to just 36% of private-sector workers by 2012. People weren't opting in, so the government made them opt out instead. Inertia, which had been keeping people out, was flipped to keep people in.

It worked. Workplace pension participation jumped to over 85% of eligible employees. Millions of people who would have reached retirement with nothing beyond the State Pension now have a pot growing. As a piece of behavioural policy design, it's hard to fault.

But auto-enrolment created a practical problem: if you're automatically enrolling 10 million people who never actively chose to save, you can't then ask each of them to build a personal investment strategy. Most won't engage. Many don't have the knowledge or confidence to choose. The system needed a default — a fund that would be good enough for the majority, chosen by the scheme provider, requiring no action from the member.

That compromise was necessary. And for the portion of the population who will never look at their pension, it's vastly better than the alternative of sitting in cash or not being invested at all. But "good enough for the majority" means it's not right for anyone in particular.

According to the Department for Work and Pensions, around 90% of auto-enrolled members remain in their scheme's default fund. That's roughly 20 million people whose retirement savings are invested in a strategy they didn't choose, may not understand, and have never reviewed.

Then came the pension freedoms. In 2015, George Osborne's reforms gave people genuine flexibility — the right to access their defined contribution pots however they wanted from age 55, instead of being effectively forced into an annuity. It was the second major pension reform in three years, and between them, auto-enrolment and pension freedoms transformed the landscape.

But the two reforms pull in opposite directions. Auto-enrolment puts people into default funds designed around the old model — the assumption that at retirement, you'll buy an annuity with your pot. Pension freedoms mean the majority of people now do something completely different. The default funds haven't caught up. They're still de-risking toward an annuity purchase that most members will never make.

How Default Funds Work

Most workplace pension defaults are some form of target date or lifestyle strategy. The concept is simple: the fund adjusts its asset allocation over time based on when you're expected to retire.

When retirement is decades away, the fund holds mostly equities — the idea being that you have time to ride out volatility and capture higher long-term returns. As you approach your target retirement date, the fund gradually shifts toward bonds, cash, and other lower-risk assets. This transition is called the "glide path."

The theory is sound. Younger investors can tolerate more risk. Older investors need more stability. A fund that automatically adjusts saves people from having to make decisions they're not equipped to make.

But the theory breaks down when you look at how it's actually implemented — and who it's designed for.

The One-Size-Fits-All Problem

A default fund has to make assumptions about you. It assumes when you'll retire. It assumes how much risk you can tolerate. It assumes what you'll do with your money at retirement — buy an annuity, enter drawdown, or take cash. It assumes you have no other pensions, no ISA, no property wealth, no partner with their own retirement savings.

Every one of these assumptions is wrong for a significant proportion of members.

The retirement age assumption

Most default funds target a retirement age of 65 or 67 — aligned with the State Pension age. But retirement ages vary enormously. Some people plan to work until 70. Others want to stop at 55. The default fund doesn't know which you are, so it picks the middle and applies the same glide path to everyone.

Someone planning to retire at 57 whose default fund is de-risking toward 67 has their money sitting in equities for a decade longer than their timeline suggests — taking on volatility that may not be appropriate given how soon they'll need the money. Conversely, someone planning to work until 70 may find the fund shifting into bonds and cash years before they need it to, potentially giving up returns that a longer timeline could have accommodated.

The drawdown vs annuity assumption

This is where the biggest damage is done. When target date funds were originally designed, the assumption was that at retirement, you'd use your pot to buy an annuity — a guaranteed income for life. The glide path was built to deliver a stable pot value at the point of purchase, which is why it shifts heavily into bonds and cash near the target date.

But since the pension freedoms of 2015, the majority of UK retirees entering drawdown don't buy an annuity. They keep their money invested and withdraw from it over time. According to FCA retirement income data, drawdown sales outnumbered annuity sales by roughly four to one in 2024-25 — around 350,000 drawdown entries compared to 88,000 annuity purchases.

For someone going into drawdown, the investment horizon doesn't end at retirement — it could extend another 20-30 years. De-risking heavily into cash and bonds at 65 may not be appropriate if the money needs to last until 90. A 25-year portfolio moved into assets that have historically struggled to keep pace with inflation over that kind of horizon faces a different kind of risk — the risk of the pot not lasting.

The default fund doesn't know your plan. It assumes the old model — and for the majority of people, the old model no longer applies.

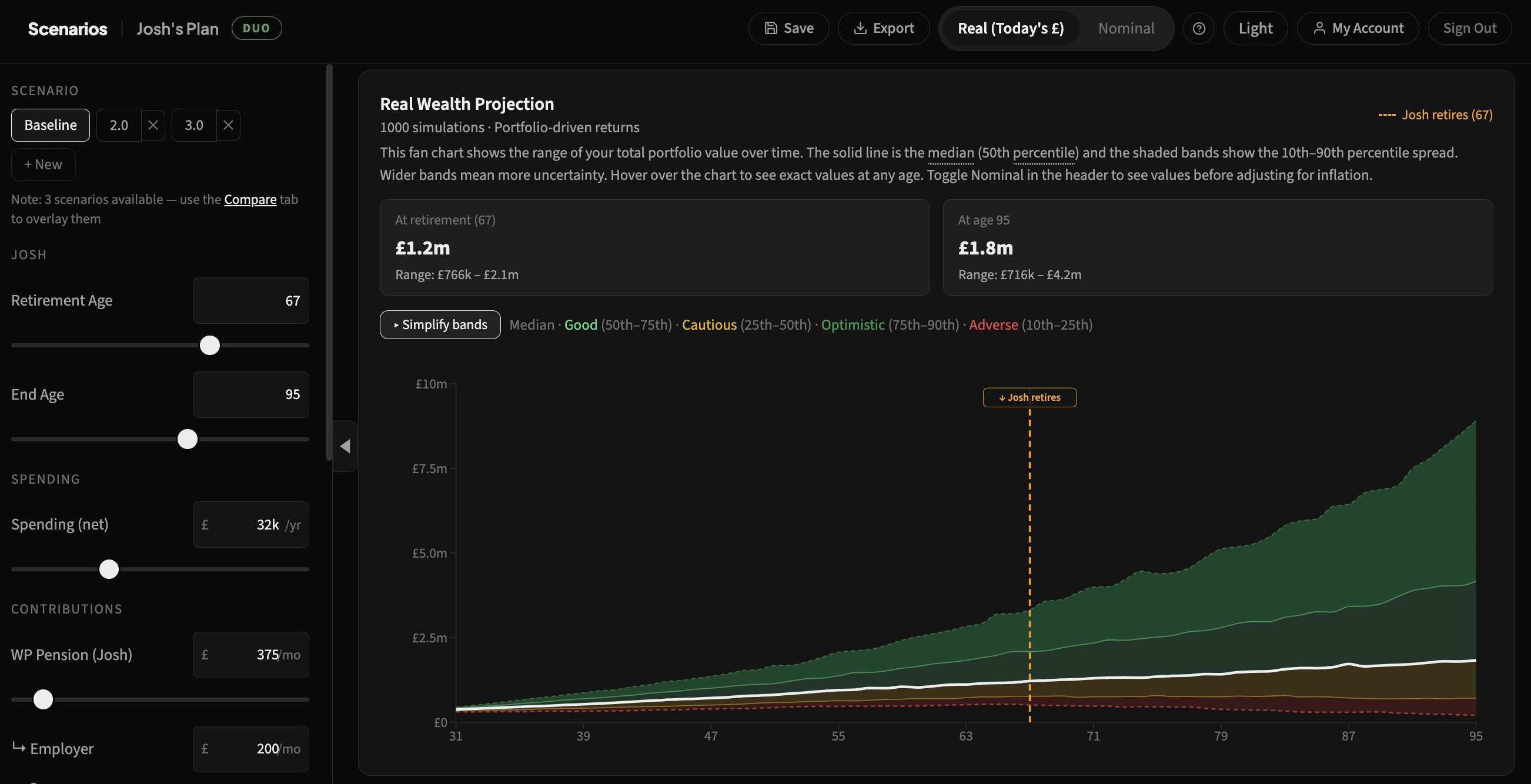

See how asset allocation shifts your outcome

Scenarios models thousands of possible futures for your exact retirement timeline — showing you how different equity/bond splits change your probability of success.

The Performance Cost of Playing It Safe

Default funds are designed to be defensible, not optimal. The pension provider's primary concern is that no member suffers a dramatic loss close to retirement — because that generates complaints, regulatory scrutiny, and reputational damage. The easiest way to avoid that is to de-risk aggressively.

The result is that most default funds are significantly more conservative than they need to be for the average member — particularly in the final 10-15 years before retirement.

Research from the Pensions Policy Institute found that a typical default strategy — shifting from 60-80% equities to 25% equities over the final 15 years — can reduce the final pot by 10-20% compared to maintaining a higher equity allocation throughout. On a £200,000 pot, that's £20,000-£40,000 less at retirement.

The WTW (formerly Willis Towers Watson) Global Pension Assets Study has consistently shown that schemes with higher equity allocations in their growth phase deliver materially better long-term outcomes. The median UK default fund returned around 7-8% annualised over the decade to 2025, but the top-quartile funds — those that maintained higher equity allocations for longer — returned 9-10%. Over 30 years of contributions, that 1-2% annual difference compounds into a gap of £50,000-£100,000 or more.

The irony is that by trying to protect everyone, default funds end up shortchanging most people. The cautious glide path is optimal for a narrow subset of members — those retiring at exactly the target date, buying an annuity, with no other assets. Everyone else pays the price for that caution.

What's Actually in Your Default Fund

Most people have no idea what their default pension fund holds. They see a name like "Retirement Plan 2045" or "Balanced Lifestyle Fund" and assume someone competent is handling it.

In practice, the holdings are fairly predictable: a mix of global equities, UK government bonds, corporate bonds, and some cash. Some include small allocations to property, infrastructure, or commodities. The equity portion is typically a passive global tracker, weighted heavily toward US large-cap stocks — which means your pension has significant exposure to American technology companies, whether or not that's appropriate for your situation.

The bond allocation is usually UK gilts and investment-grade corporate bonds. In a rising interest rate environment — like the one the UK has experienced since 2022 — bond values fall. Members who were de-risked into bonds during 2022-2023 saw their "safe" allocation lose 15-25% of its value. UK gilts had their worst year in over a century in 2022.

That's not a failure of bonds as an asset class — it's a failure of the assumption that bonds are always "safe." They're less volatile than equities on average, but they're not risk-free, and in certain environments they can be worse. A default fund that mechanically shifts into bonds regardless of the interest rate environment isn't managing risk — it's following a script.

The People Who Are Worst Served

Default funds work least well for people whose circumstances diverge most from the average. That includes:

Higher earners. Someone earning £80,000 with a £400,000 pension pot has different risk capacity and tax considerations from someone earning £25,000 with a £30,000 pot. The default fund treats them identically.

People with multiple pensions. If you have three pension pots from different employers, each one is de-risking independently. Your overall portfolio allocation becomes increasingly conservative because each fund is individually dialling down risk without knowing about the others. You might end up with 80% of your total retirement savings in bonds and cash — far more conservative than necessary.

People with significant other assets. Someone with £200,000 in ISAs, a paid-off house, and a full State Pension entitlement may have a pension pot that doesn't need to do all the heavy lifting — which could change the risk profile that's appropriate. The default fund doesn't know any of this.

People retiring early. Someone planning to retire at 55 whose default fund targets 67 is in growth-phase equities at a point when the fund's glide path hasn't yet begun to adjust. By the time the fund starts de-risking, they may already be years into retirement.

People retiring late. Someone planning to work until 70 may find they've been in increasingly conservative assets for years longer than their timeline requires — potentially giving up returns that a longer horizon could have accommodated.

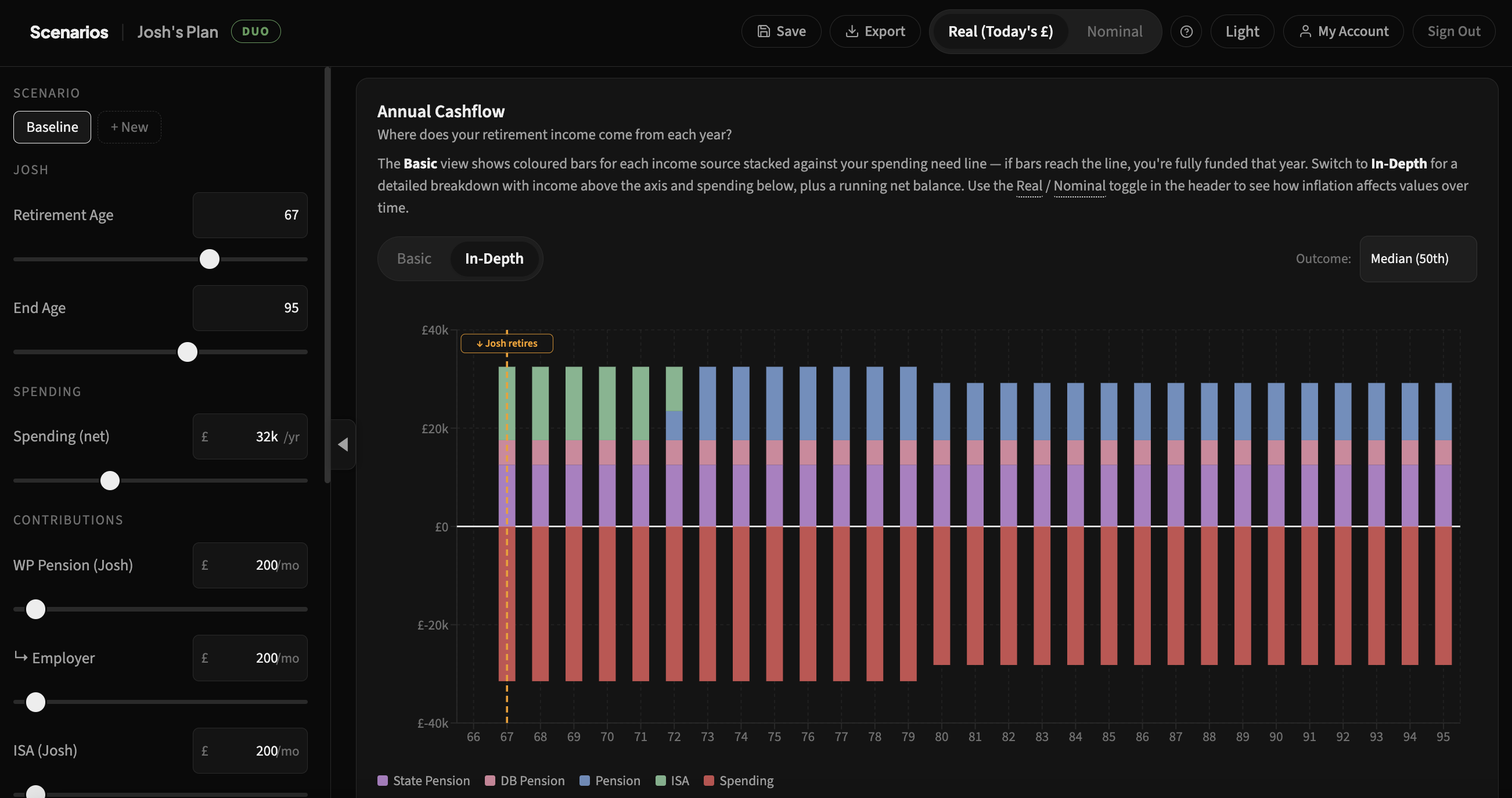

Your full financial picture in one place

Default funds don't know about your ISA, your partner's pension, or your rental income. Scenarios lets you model everything together — so your asset allocation reflects your actual situation.

The Numbers That Should Worry You

The Pension Policy Institute's 2025 DC Future Book reported that the median UK defined contribution pot at retirement is approximately £45,000. That's enough to generate roughly £2,000-£2,500 per year in drawdown income — barely enough to supplement the State Pension.

Part of this is a contribution problem — people simply aren't saving enough. The minimum auto-enrolment contribution of 8% (with at least 3% from the employer) is widely acknowledged to be insufficient. The PLSA's Retirement Living Standards suggest that a "moderate" retirement lifestyle requires around £31,700 per year for a single person — which, after the State Pension, means generating roughly £19,700 per year from private savings.

But part of it is an investment problem. If default funds are delivering 1-2% less per year than a well-chosen alternative — and for many members, over many years, they are — that shortfall compounds into a significantly smaller pot at retirement. On a 30-year savings horizon with £300/month contributions, the difference between 7% and 8.5% annualised returns is approximately £75,000.

That's not a rounding error. That's years of retirement income.

The Three Questions Worth Asking

None of this is advice — everyone's situation is different, and the right answer depends on circumstances that only you (and potentially a financial adviser) can assess. But there are three questions that are worth understanding, regardless of what you decide to do with the answers.

1. Where is it invested?

Most pension providers show your current fund allocation on their website — the split between equities, bonds, cash, and other assets. Many people have never looked. Just knowing what you own is a starting point.

2. What risk are you actually taking?

Risk isn't just about volatility. There's also the risk that a pot won't be large enough to fund the retirement someone wants. Being too cautious can be as costly as being too aggressive — but the right balance depends entirely on the individual's total financial picture, not a generic model.

3. What returns has the fund delivered?

Default funds publish their historical performance. Comparing that to what a pot would need to grow to — given contribution levels, timeline, and spending goals — at least makes the gap visible. It's easier to make informed decisions when the numbers are clear.

Default Funds Aren't the Villain

None of this is an argument against default funds existing. For the portion of the population who will never engage with their pension — and that's a significant number — a default fund is vastly better than not being invested at all. Auto-enrolment combined with default investment strategies has brought millions of people into pension saving who would otherwise have nothing. That's a genuine achievement.

The issue isn't that defaults are bad. It's that they're generic by design. They have to be — they're built for millions of people at once. The question is whether accepting a generic strategy is the right trade-off for any given individual, and the only way to know that is to understand what the default is actually doing and how it compares to what that person's situation calls for.

Most pension providers offer a range of funds beyond the default — different risk profiles, different equity allocations, different regional exposures. Whether any of those alternatives would be more appropriate depends entirely on individual circumstances. But making that assessment starts with understanding the current position.

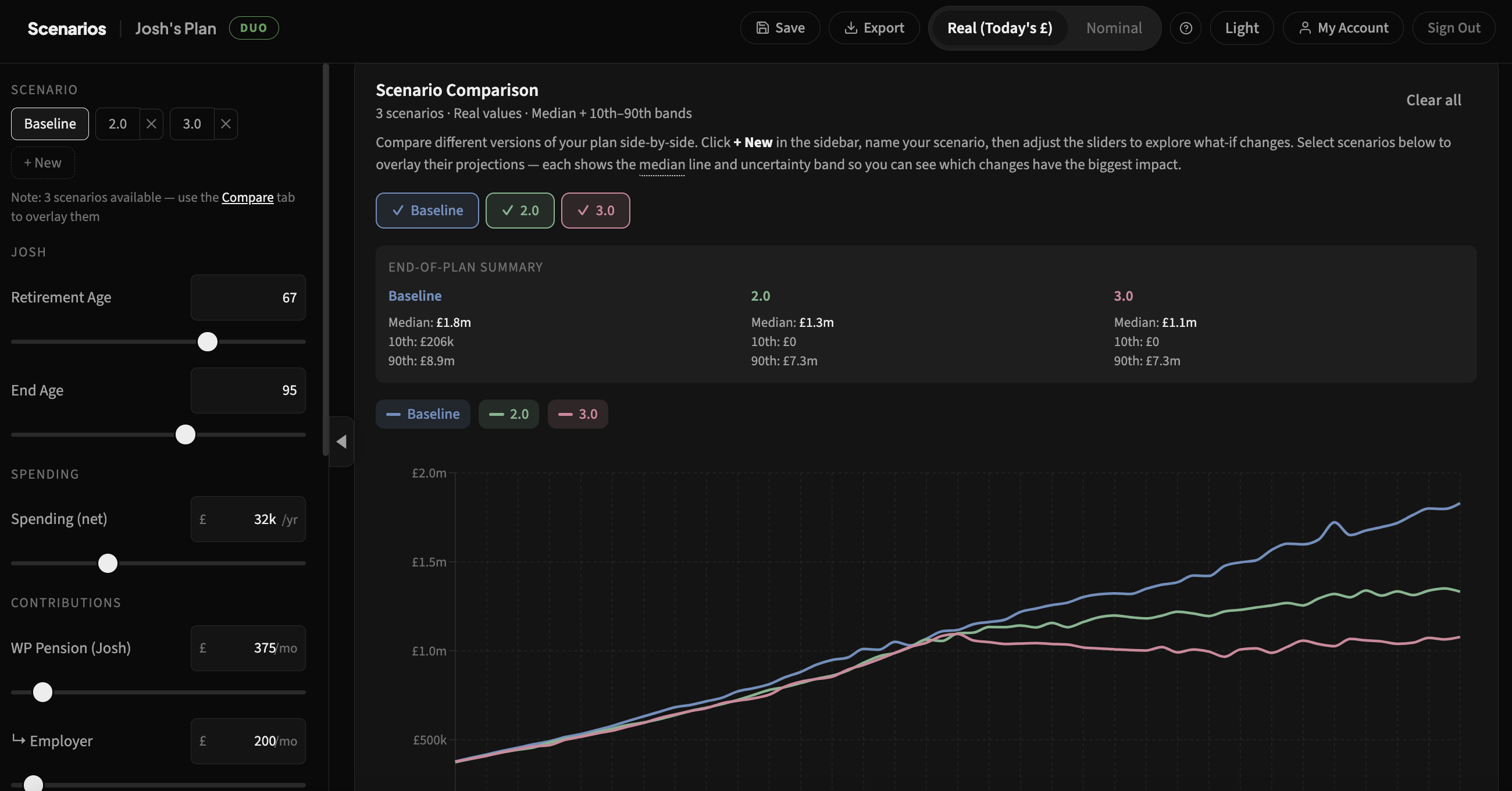

If you're curious about how different assumptions — retirement age, contribution levels, asset allocation, market conditions — affect long-term outcomes, you can build a free scenario and explore the range of possibilities. It won't tell you what to do, but it will show you what the numbers look like.

Further Reading

- Department for Work and Pensions (2025). Automatic Enrolment Evaluation Report. DWP.

- Pensions Policy Institute (2025). The DC Future Book: In Association with Columbia Threadneedle Investments. PPI.

- FCA (2025). Retirement Income Market Data 2024/25. Financial Conduct Authority.

- PLSA (2025). Retirement Living Standards. Pensions and Lifetime Savings Association.

- WTW (2025). Global Pension Assets Study. Willis Towers Watson.

- Byrne, A., Dowd, K., Blake, D. & Cairns, A. (2007). "Default Funds in UK Defined-Contribution Plans." Financial Analysts Journal, 63(4), 40–51.

- Pensions Regulator (2025). Code of Practice: Investment Governance. TPR.gov.uk.

Enter your email to continue reading

Get full access to this article and new posts from The Daily Interest delivered to your inbox.

By subscribing you agree to receive blog updates from The Daily Interest. You can unsubscribe at any time. See our Privacy Policy.

Run 1,000 Monte Carlo simulations across your pensions, ISAs, and investments — completely free.

Get Started Free

10 Reasons Your Retirement Number Is Probably Wrong

Most retirement numbers come from a rule of thumb that was never built for you. Here are ten reasons the figure in your head is likely off, and what actually moves the answer.

UK Annuity Rates Are Back: What 2026's Higher Rates Mean for Retirees

After a decade of being written off, annuity rates have climbed to levels not seen since 2008. Here's what that changes for retirement planning.